Note

Click here to download the full example code or to run this example in your browser via Binder

Tuning a scikit-learn estimator with skopt¶

Gilles Louppe, July 2016 Katie Malone, August 2016 Reformatted by Holger Nahrstaedt 2020

If you are looking for a sklearn.model_selection.GridSearchCV replacement checkout

Scikit-learn hyperparameter search wrapper instead.

Problem statement¶

Tuning the hyper-parameters of a machine learning model is often carried out

using an exhaustive exploration of (a subset of) the space all hyper-parameter

configurations (e.g., using sklearn.model_selection.GridSearchCV), which

often results in a very time consuming operation.

In this notebook, we illustrate how to couple gp_minimize with sklearn’s

estimators to tune hyper-parameters using sequential model-based optimisation,

hopefully resulting in equivalent or better solutions, but within less

evaluations.

Note: scikit-optimize provides a dedicated interface for estimator tuning via

BayesSearchCV class which has a similar interface to those of

sklearn.model_selection.GridSearchCV. This class uses functions of skopt to perform hyperparameter

search efficiently. For example usage of this class, see

Scikit-learn hyperparameter search wrapper

example notebook.

print(__doc__)

import numpy as np

Objective¶

To tune the hyper-parameters of our model we need to define a model, decide which parameters to optimize, and define the objective function we want to minimize.

from sklearn.datasets import load_boston

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.model_selection import cross_val_score

boston = load_boston()

X, y = boston.data, boston.target

n_features = X.shape[1]

# gradient boosted trees tend to do well on problems like this

reg = GradientBoostingRegressor(n_estimators=50, random_state=0)

Next, we need to define the bounds of the dimensions of the search space we want to explore and pick the objective. In this case the cross-validation mean absolute error of a gradient boosting regressor over the Boston dataset, as a function of its hyper-parameters.

from skopt.space import Real, Integer

from skopt.utils import use_named_args

# The list of hyper-parameters we want to optimize. For each one we define the

# bounds, the corresponding scikit-learn parameter name, as well as how to

# sample values from that dimension (`'log-uniform'` for the learning rate)

space = [Integer(1, 5, name='max_depth'),

Real(10**-5, 10**0, "log-uniform", name='learning_rate'),

Integer(1, n_features, name='max_features'),

Integer(2, 100, name='min_samples_split'),

Integer(1, 100, name='min_samples_leaf')]

# this decorator allows your objective function to receive a the parameters as

# keyword arguments. This is particularly convenient when you want to set

# scikit-learn estimator parameters

@use_named_args(space)

def objective(**params):

reg.set_params(**params)

return -np.mean(cross_val_score(reg, X, y, cv=5, n_jobs=-1,

scoring="neg_mean_absolute_error"))

Optimize all the things!¶

With these two pieces, we are now ready for sequential model-based optimisation. Here we use gaussian process-based optimisation.

from skopt import gp_minimize

res_gp = gp_minimize(objective, space, n_calls=50, random_state=0)

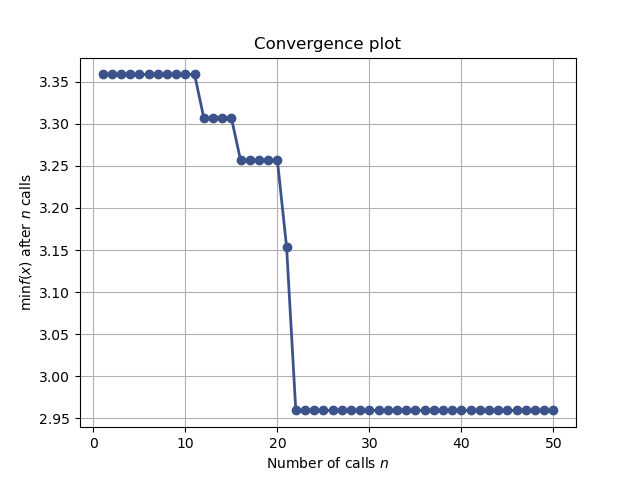

"Best score=%.4f" % res_gp.fun

Out:

'Best score=2.9593'

print("""Best parameters:

- max_depth=%d

- learning_rate=%.6f

- max_features=%d

- min_samples_split=%d

- min_samples_leaf=%d""" % (res_gp.x[0], res_gp.x[1],

res_gp.x[2], res_gp.x[3],

res_gp.x[4]))

Out:

Best parameters:

- max_depth=5

- learning_rate=0.112019

- max_features=13

- min_samples_split=51

- min_samples_leaf=1

Convergence plot¶

from skopt.plots import plot_convergence

plot_convergence(res_gp)

Out:

<AxesSubplot:title={'center':'Convergence plot'}, xlabel='Number of calls $n$', ylabel='$\\min f(x)$ after $n$ calls'>

Total running time of the script: ( 0 minutes 29.253 seconds)

Estimated memory usage: 32 MB