Note

Click here to download the full example code or to run this example in your browser via Binder

Tuning a scikit-learn estimator with skopt¶

Gilles Louppe, July 2016 Katie Malone, August 2016 Reformatted by Holger Nahrstaedt 2020

If you are looking for a sklearn.model_selection.GridSearchCV replacement checkout

Scikit-learn hyperparameter search wrapper instead.

Problem statement¶

Tuning the hyper-parameters of a machine learning model is often carried out

using an exhaustive exploration of (a subset of) the space all hyper-parameter

configurations (e.g., using sklearn.model_selection.GridSearchCV), which

often results in a very time consuming operation.

In this notebook, we illustrate how to couple gp_minimize with sklearn’s

estimators to tune hyper-parameters using sequential model-based optimisation,

hopefully resulting in equivalent or better solutions, but within fewer

evaluations.

Note: scikit-optimize provides a dedicated interface for estimator tuning via

BayesSearchCV class which has a similar interface to those of

sklearn.model_selection.GridSearchCV. This class uses functions of skopt to perform hyperparameter

search efficiently. For example usage of this class, see

Scikit-learn hyperparameter search wrapper

example notebook.

print(__doc__)

import numpy as np

Objective¶

To tune the hyper-parameters of our model we need to define a model, decide which parameters to optimize, and define the objective function we want to minimize.

from sklearn.datasets import load_boston

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.model_selection import cross_val_score

boston = load_boston()

X, y = boston.data, boston.target

n_features = X.shape[1]

# gradient boosted trees tend to do well on problems like this

reg = GradientBoostingRegressor(n_estimators=50, random_state=0)

Out:

/home/circleci/miniconda/envs/testenv/lib/python3.9/site-packages/scikit_learn-1.0-py3.9-linux-x86_64.egg/sklearn/utils/deprecation.py:87: FutureWarning: Function load_boston is deprecated; `load_boston` is deprecated in 1.0 and will be removed in 1.2.

The Boston housing prices dataset has an ethical problem. You can refer to

the documentation of this function for further details.

The scikit-learn maintainers therefore strongly discourage the use of this

dataset unless the purpose of the code is to study and educate about

ethical issues in data science and machine learning.

In this case special case, you can fetch the dataset from the original

source::

import pandas as pd

import numpy as np

data_url = "http://lib.stat.cmu.edu/datasets/boston"

raw_df = pd.read_csv(data_url, sep="\s+", skiprows=22, header=None)

data = np.hstack([raw_df.values[::2, :], raw_df.values[1::2, :2]])

target = raw_df.values[1::2, 2]

Alternative datasets include the California housing dataset (i.e.

func:`~sklearn.datasets.fetch_california_housing`) and the Ames housing

dataset. You can load the datasets as follows:

from sklearn.datasets import fetch_california_housing

housing = fetch_california_housing()

for the California housing dataset and:

from sklearn.datasets import fetch_openml

housing = fetch_openml(name="house_prices", as_frame=True)

for the Ames housing dataset.

warnings.warn(msg, category=FutureWarning)

Next, we need to define the bounds of the dimensions of the search space we want to explore and pick the objective. In this case the cross-validation mean absolute error of a gradient boosting regressor over the Boston dataset, as a function of its hyper-parameters.

from skopt.space import Real, Integer

from skopt.utils import use_named_args

# The list of hyper-parameters we want to optimize. For each one we define the

# bounds, the corresponding scikit-learn parameter name, as well as how to

# sample values from that dimension (`'log-uniform'` for the learning rate)

space = [Integer(1, 5, name='max_depth'),

Real(10**-5, 10**0, "log-uniform", name='learning_rate'),

Integer(1, n_features, name='max_features'),

Integer(2, 100, name='min_samples_split'),

Integer(1, 100, name='min_samples_leaf')]

# this decorator allows your objective function to receive a the parameters as

# keyword arguments. This is particularly convenient when you want to set

# scikit-learn estimator parameters

@use_named_args(space)

def objective(**params):

reg.set_params(**params)

return -np.mean(cross_val_score(reg, X, y, cv=5, n_jobs=-1,

scoring="neg_mean_absolute_error"))

Optimize all the things!¶

With these two pieces, we are now ready for sequential model-based optimisation. Here we use gaussian process-based optimisation.

from skopt import gp_minimize

res_gp = gp_minimize(objective, space, n_calls=50, random_state=0)

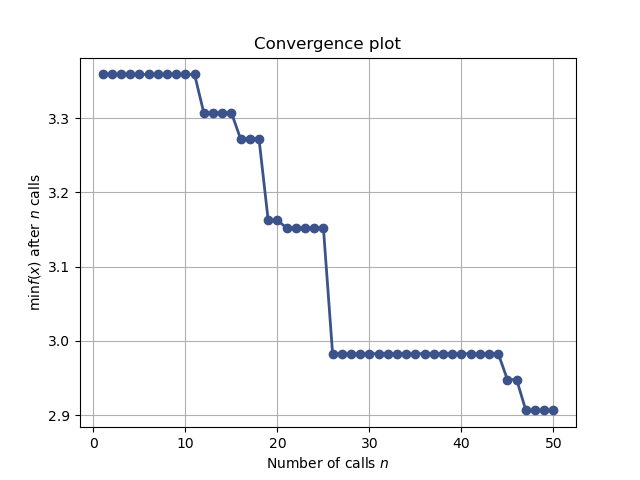

"Best score=%.4f" % res_gp.fun

Out:

'Best score=2.9062'

print("""Best parameters:

- max_depth=%d

- learning_rate=%.6f

- max_features=%d

- min_samples_split=%d

- min_samples_leaf=%d""" % (res_gp.x[0], res_gp.x[1],

res_gp.x[2], res_gp.x[3],

res_gp.x[4]))

Out:

Best parameters:

- max_depth=5

- learning_rate=0.143650

- max_features=9

- min_samples_split=100

- min_samples_leaf=1

Convergence plot¶

from skopt.plots import plot_convergence

plot_convergence(res_gp)

Out:

<AxesSubplot:title={'center':'Convergence plot'}, xlabel='Number of calls $n$', ylabel='$\\min f(x)$ after $n$ calls'>

Total running time of the script: ( 0 minutes 28.593 seconds)

Estimated memory usage: 35 MB